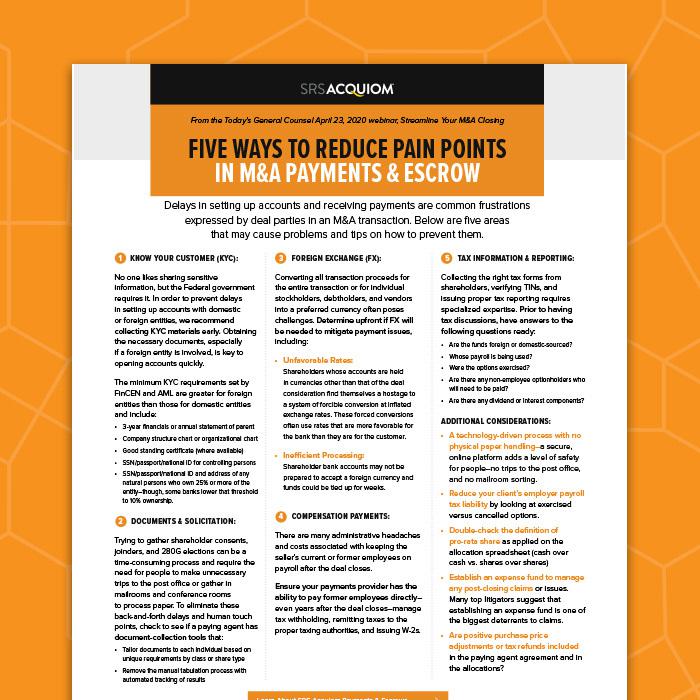

Delays in setting up accounts and receiving payments are common frustrations expressed by deal parties in an M&A transaction. Below are five areas that may cause problems and tips on how to prevent them.

1. Know Your Customer (KYC):

No one likes sharing sensitive information, but the Federal government requires it. In order to prevent delays in setting up accounts with domestic or foreign entities, we recommend collecting KYC materials early. Obtaining the necessary documents, especially if a foreign entity is involved, is key to opening accounts quickly. The minimum KYC requirements set by FinCEN and AML are greater for foreign entities than those for domestic entities and include:

- 3-year financials or annual statement of parent

- Company structure chart or organizational chart

- Good standing certificate (where available)

- SSN/passport/national ID for controlling persons

- SSN/passport/national ID and address of any natural persons who own 25% or more of the entity–though, some banks lower that threshold to 10% ownership.

2. Documents & Solicitation:

Trying to gather shareholder consents, joinders, and 280G elections can be a time-consuming process and require the need for people to make unnecessary trips to the post office or gather in mailrooms and conference rooms to process paper. To eliminate these back-and-forth delays and human touch points, check to see if a paying agent has document-collection tools that:

- Tailor documents to each individual based on unique requirements by class or share type

- Remove the manual tabulation process with automated tracking of results

3. Foreign Exchange (FX):

Converting all transaction proceeds for the entire transaction or for individual stockholders, debtholders, and vendors into a preferred currency often poses challenges. Determine upfront if FX will be needed to mitigate payment issues, including:

• Unfavorable Rates:

Shareholders whose accounts are held in currencies other than that of the deal consideration find themselves a hostage to a system of forcible conversion at inflated exchange rates. These forced conversions often use rates that are more favorable for the bank than they are for the customer.

• Inefficient Processing:

Shareholder bank accounts may not be prepared to accept a foreign currency and funds could be tied up for weeks.

4. Compensation Payments:

There are many administrative headaches and costs associated with keeping the seller’s current or former employees on payroll after the deal closes.

Ensure your payments provider has the ability to pay former employees directly–even years after the deal closes–manage tax withholding, remitting taxes to the proper taxing authorities, and issuing W-2s.

5. Tax Information & Reporting:

Collecting the right tax forms from shareholders, verifying TINs, and issuing proper tax reporting requires specialized expertise. Prior to having tax discussions, have answers to the following questions ready:

- Are the funds foreign or domestic-sourced?

- Whose payroll is being used?

- Were the options exercised?

- Are there any non-employee optionholders who will need to be paid?

- Are there any dividend or interest components?

Additional Considerations:

- A technology-driven process with no physical paper handling–a secure, online platform adds a level of safety for people–no trips to the post office, and no mailroom sorting

- Reduce your client’s employer payroll tax liability by looking at exercised versus cancelled options.

- Double-check the definition of pro-rata share as applied on the allocation spreadsheet (cash over cash vs. shares over shares)

- Establish an expense fund to manage any post-closing claims or issues. Many top litigators suggest that establishing an expense fund is one of the biggest deterrents to claims.

- Are positive purchase price adjustments or tax refunds included in the paying agent agreement and in the allocations?