Format

Deal Terms Analysis

Indemnification

Deal Terms for M&A Escrows - Statistics and Key Findings

Deal Terms Analysis

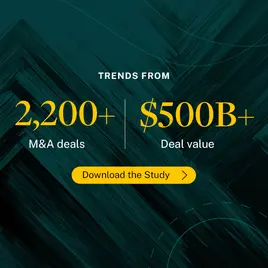

M&A Deals: Key Trends and Highlights from the SRS Acquiom M&A 2025 Deal Terms Study

Deal Terms Analysis

2025 M&A Deal Terms Study

Deal Terms Analysis

2025 Working Capital Purchase Price Adjustment Study

Deal Terms Analysis

Life Sciences

Bio/Pharma M&A: Earnout Achievement Insights

Deal Terms Analysis

M&A Deal Terms: Three Trends to Watch in 2025

Deal Terms Analysis

2024 Trends in M&A Indemnification Claims and Earnouts

Deal Terms Analysis

Lower Middle Market M&A Deals: What Makes Them Different?

Deal Terms Analysis

2024 M&A Deal Terms Special Report: Lower Middle-Market Deals

Deal Terms Analysis

2024 M&A Claims Insights Report

Indemnification

Deal Terms Analysis

2024 RWI Highlights: Effect of Reps and Warranties Insurance on M&A Deal Terms

Deal Terms Analysis

2024 M&A Deal Terms: Highlights for M&A Advisors

Deal Terms Analysis

2024 M&A Deal Terms Study

Deal Terms Analysis

2024 M&A Working Capital PPA Study

Deal Terms Analysis

M&A Earnouts: Be Prepared for 2024

Shareholder Representation

Deal Terms Analysis

M&A Purchase Price Adjustments Are Common Yet Complex

Deal Terms Analysis

Valuation Disconnects Driving a Spike in Earnouts in M&A

Deal Terms Analysis

2023 Lower Middle-Market Mergers & Acquisitions Deals Report

Deal Terms Analysis

Life Sciences

2023 SRS Acquiom Life Sciences M&A Study

Deal Terms Analysis

2023 M&A Deal Terms and Trends for Private Equity Buyers

Deal Terms Analysis

Technology M&A Deal Terms and Trends

Deal Terms Analysis

Indemnification

Effect of Representations and Warranties Insurance on Deal Terms

Deal Terms Analysis

Private M&A Deal Terms: An SRS Acquiom Quick Guide for M&A Advisors

Deal Terms Analysis

Tools and Tactics for Getting Deals Across the Finish Line

Deal Terms Analysis

2023 M&A Deal Terms Study

Deal Terms Analysis

M&A Trends: PPAs and Claims Activity

Deal Terms Analysis

Post-Closing M&A Claims and Purchase Price Adjustments: Where Do They Stand Heading Into 2023?

Deal Terms Analysis

Due Diligence

How M&A Advisors Use Deal Data to Improve the Due Diligence Process

Deal Terms Analysis

Indemnification

2022 M&A Claims Insights Report

Deal Terms Analysis

Life Sciences

2021 Life Sciences M&A Study

Deal Terms Analysis

2020 M&A Claims Insights Report

Deal Terms Analysis

Shareholder Representation

What to Make of the Great Hill Case – The M&A Bar is Not Yet in Agreement on How Best to Address Merger Agreement Privilege Issues

Deal Terms Analysis

2020 Review: COVID-19 Impact on M&A Transactions

Deal Terms Analysis

M&A Deal Terms & Trends Pre- & Post-COVID-19

Deal Terms Analysis

Shareholder Representation

M&A: Who Owns the Attorney-Client Privilege After Closing?

Deal Terms Analysis

2020 Buy-Side Reps and Warranties Insurance Deal Terms Update

Deal Terms Analysis

A First Look at the Impacts of Coronavirus on M&A Transactions

Deal Terms Analysis

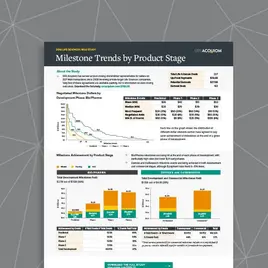

Life Sciences

Life Sciences: Milestone Trends by Product Stage

Deal Terms Analysis

Life Sciences

Life Sciences: Timeline of Milestone Payments

Deal Terms Analysis

Shareholder Representation

Addressing Target Company Privilege in Merger Agreements Five Years after Great Hill v. SIG

Deal Terms Analysis

Shareholder Representation

Beware of Exclusions When Defining Net Working Capital in M&A Transactions

Deal Terms Analysis

Life Sciences

2019 Life Sciences Study Quick Reference Guide

Deal Terms Analysis

Life Sciences

2019 Life Sciences M&A Study

Deal Terms Analysis

Shareholder Representation

Understanding Changes in Shareholder Consent Requirements

Deal Terms Analysis

Shareholder Representation

Clarifying When Attorneys’ Fees Constitute Damages

Deal Terms Analysis

Shareholder Representation

M&A Conflict Waivers

Deal Terms Analysis

Shareholder Representation

Do Carveouts to Caps Work the Way You Intend?

Deal Terms Analysis

Shareholder Representation

Definition of Purchase Price